Cov Mat R Finance

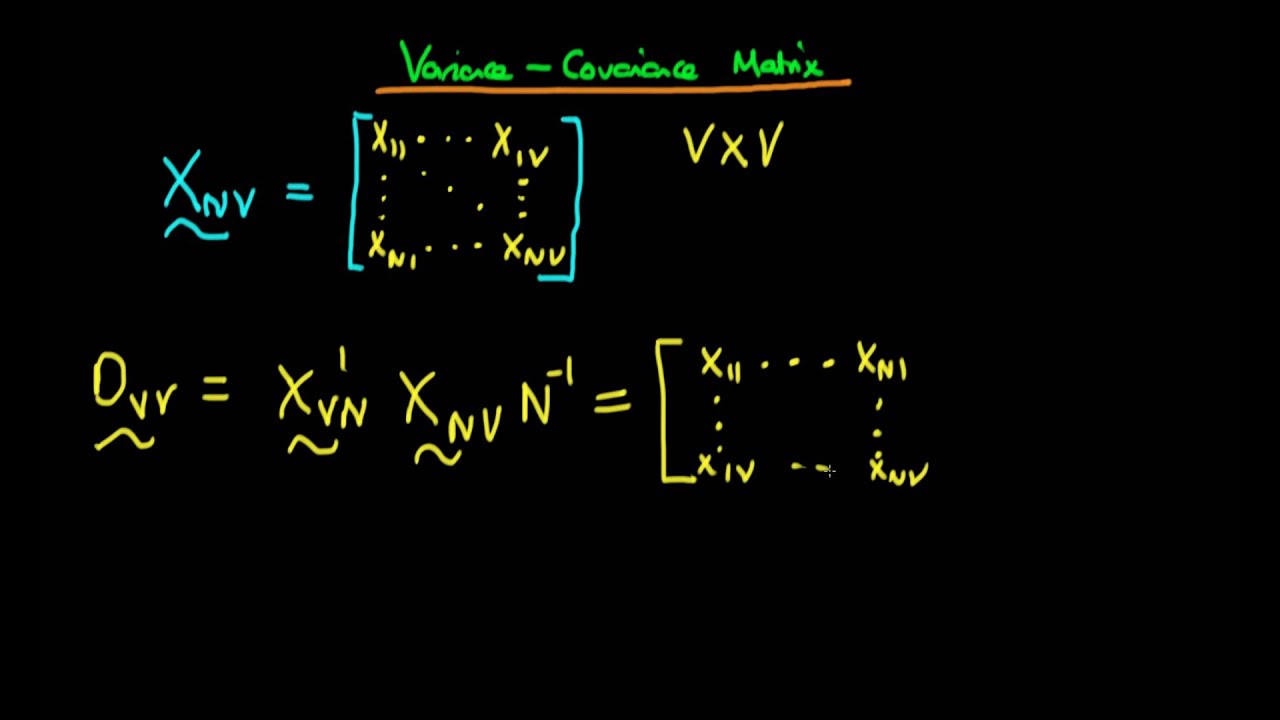

Variance Covariance Matrix Stock Price Analysis In R Corpcor Covmat In 2020 Stock Market Crash Stock Research Stock Market

Rip Robin Williams Genie We Re Gonna Miss You T Shirt By Suzeejobs R Aff Ad Williams Robin Rip Genie In 2020 Geek Quotes Classic T Shirts Geek Humor

Album Cover Artist Book Project Launches On Kickstarter Album Covers Book Projects Album

Variance Covariance Matrix Using Matrix Notation Of Factor Analysis Youtube

Toyota Yaris Hybrid R Concept Mikeshouts Yaris Toyota Toyota Hybrid

Maxpider 3d Rubber Molded Floor Mat For Volkswagen Jetta 05 10 Kagu Gray Row 1 2 Jetta Gli Volkswagen Jetta Volkswagen

Description compute global minimum variance portfolio given expected return vector and covariance matrix.

Cov mat r finance. The benn education centre. Cross covariance matrix computes the cross covariance matrix between two sets of locations for a spatial random process with a given covariance structure. Param er samp n x 1 vector of expected returns param cov mat samp n x n return covariance matrix param target return scalar target expected return param shorts logical if. Dat dat c 2 4 remove team name and ds names left in data frame names dat 1 playername mb game reshape from long to wide dat wide reshape dat direction wide idvar game timevar playername dat wide 1.

Typically the two sets are a learning set and a test set. If short sales are not allowed then the portfolio is computed numerically using the function samp solve qp from the samp quadprog package. For covariance matrix estimation three major types of factor models are included. Smart beta is what people call algorithms that construct portfolios that are intended to beat market cap weighted benchmarks without a human.

Macroeconomic factor model fundamental factor model and statistical factor model. Useful financial r snippets making smart beta portfolios in r making smart beta portfolios in r here we explore smart beta and how to build portfolios which implement smart beta in r. R functions for portfolio analysis my r functions on class webpage in portfolio r and portfolio noshorts r r packager package portfolioanalytics on r on r forge extensive collection of functions rtirme trics package fp tf lifportfolio extensive collection of functions r package quadprog solve qp for quadratic. The portfolio can allow all assets to be shorted or not allow any assets to be shorted.

Suppose our data is in dat. Type package title covariance matrix estimation and regularization for finance version 1 1 0 description estimation and regularization for covariance matrix of asset returns. The returned object is of class portfolio. Tax lien sale virtual outreach sessions.

Department of finance 311 search all nyc gov websites. Property records acris contact us. Er n x 1 vector of expected returns cov mat n x n covariance matrix of returns weights n x 1 vector of portfolio weights output is portfolio object with the following elements. Portfolio r functions for portfolio analysis to be used in introduction to computational finance financial econometrics last.

I think what you first need to do is reshape the data so that each row is a game and each column is the mb for a game for a player.

Vtec Mini Vtec Mini Mini Cooper

Invitations De Mariage Fete Rock N Roll Design Disque Wedding Party Invites Affordable Wedding Invitations Rock N Roll Wedding

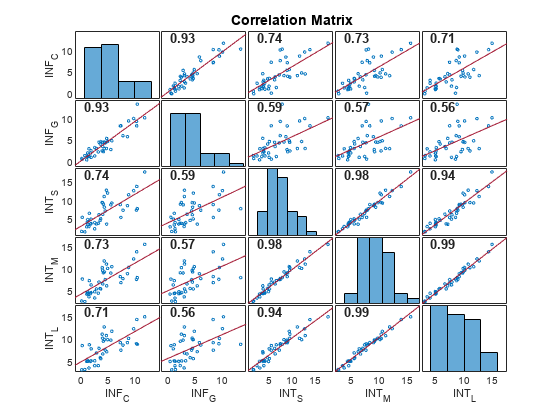

Plot Variable Correlations Matlab Corrplot

Fondos De Pantalla Simple Acrylic Paintings Aesthetic Pastel Wallpaper Aesthetic Art

How To Draw A 95 Confidence Ellipse To An Xy Scatter Plot

2019 Bmw S 1000 Rr An Icon Among Superbikes Bmw S1000rr Bmw Sport Bmw S

3 680 Mentions J Aime 19 Commentaires Alfa Romeo Thealfacollection Sur Instagram Awesome Drive Free In 2020 Alfa Romeo Gta Classic Cars Car

Mini Beachcomber 4x4 Concept Heads To Detroit Auto Show New Photos Added Carscoops Mini Cooper Mini Cars Mini

Minimalist Graphic Design Minimalist Graphic Design Graphic Design Design Shack

To Be Lucky Luck Quotes Good Luck Quotes Wonderful Words

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctdiuliqmdrtoedcavl4trt5fuhhlz3adyqza Usqp Cau

Pin On Marine Electronics Products

Estimation Of Covariance Matrices Wikipedia

Pin By Kathleen Brewer On Bjj In 2020 Jiu Jitsu Tattoo Jiu Jitsu Bjj

40 Stunning Minimalistic Book Cover Designs Book Cover Cover Design Minimalist

Http Past Rinfinance Com Agenda 2009 Yollin Slides Pdf

Pecop Blog Read Physiology Educators Perspectives On Educational Issues Including Education Transformation Developing And Using Core Concepts And Competencies Using Evidence Based Innovations In Student Centered Learning Aligning Teaching And

15 Outstanding Wall Art Ideas Inspired By Optical Illusions Kargah Olom 3d Wall Painting Optical Illusions 3d Wall Art

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsxjyhwjgbeknxy2cbx6kta5ivyipbssp Mkd 89tcb28043rne Usqp Cau

Unity In Action 2nd Edition Python Javascript Angular Angularjs Reactjs Vuejs Webdev Perl Ruby C Csharp Game Development Free Books Online Unity

Pin On Books Within Books

Pdf Modeling Univariate And Multivariate Stochastic Volatility In R With Stochvol And Factorstochvol

Uekg7bhv32ifkm

Used 2018 Volkswagen Golf R For Sale Near Me Edmunds

Used 2019 Volkswagen Golf R For Sale In Fort Lauderdale Fl Edmunds

Skyline Soul Miniature And Cute Tattoo By Akash Chandani Email For Appointments Skinmachineteam Gmail Com Www Cute Tattoos Girl Tattoos Tattoo Quotes

Pdf Cts An R Package For Continuous Time Autoregressive Models Via Kalman Filter

Vedrpa0pjym8um

Album Cover Artist Book Project Launches On Kickstarter Album Covers Book Projects Album

Pdf The Making Of Good Financial Regulation Towards A Policy Response To Regulatory Capture

Https Web Wpi Edu Pubs Etd Available Etd 080614 144242 Unrestricted Chen Huanting Pca 2014 07 31 Final Version Pdf

Oxidoreductases Generate Hydrogen Peroxide That Drives Iron Dependent Lipid Peroxidation During Ferroptosis Biorxiv

Used Volkswagen Golf R For Sale In Orange Ca Edmunds

Used 2010 Nissan Gt R For Sale Near Me Edmunds

Coronavirus Information

Https Www Ams Org Journals Notices 200208 200208fullissue Pdf

Cool Chevrolet 2017 67 Camaro Cool Rides Check More At Http Carboard Pro Cars Gallery 2017 Chevrolet 2017 67 Camaro Cool Ri Camaro Dream Cars Muscle Cars

Http Www P12 Nysed Gov Sss Schoolhealth Schoolhealthservices Coronavirus Covid 19 P 12 School Guidance Pdf

Punching Shear Behavior Of Two Way Coral Reef Sand Concrete Slab Reinforced With Bfrp Composites Sciencedirect

Album Cover Artist Book Project Launches On Kickstarter Album Covers Book Projects Album

Is The Coronavirus In Bible Prophecy Facing Uncertain Times With David Jeremiah Youtube

Https Kynewsgroup Com Clients Kynewsgroup Bcn08132020 Pdf